Rise in Delinquent Commercial Real Estate Mortgages: Analyzing the Impact of Forbearance Strategies

By Wolf Richter for WOLF STREET

The commercial real estate (CRE) landscape faced significant turmoil in August, particularly within the office and multifamily sectors. This downturn occurred despite the widespread implementation of extend-and-pretend and forbearance strategies, aimed at alleviating loan delinquencies in anticipation of improved economic conditions.

Alarming Delinquency Rates in Office Mortgages

The delinquency rate for office mortgages that are part of commercial mortgage-backed securities (CMBS) surged to an unprecedented 11.7% in August. This figure not only marks a new high but also surpasses the delinquency peak observed during the Financial Crisis, which stood at 10.7%, according to Trepp, a leading analytics firm in CMBS tracking.

As recently as December 2022, the delinquency rate for office loans was merely 1.6%. The escalation of over 10 percentage points since then underscores the pervasive strains that the sector is enduring.

Older office buildings are particularly vulnerable, as high vacancy rates in modern structures encourage tenants to relocate. This ongoing “flight to quality” further exacerbates challenges for their less desirable counterparts.

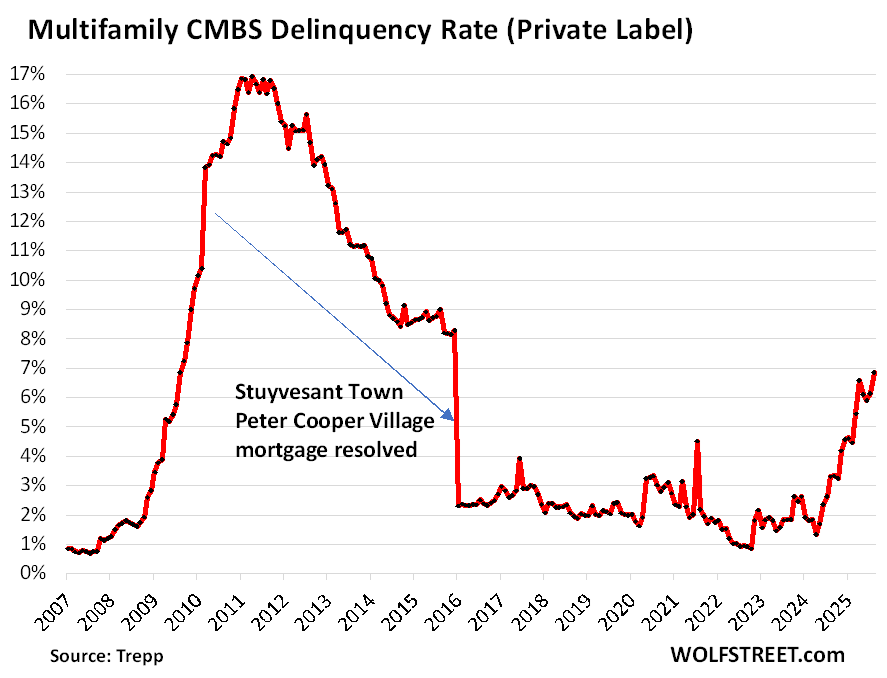

Multifamily Mortgages Also Facing Distress

Meanwhile, the multifamily sector isn’t faring well either. The delinquency rate for multifamily CMBS rose to 6.9%, marking the worst levels since December 2015. To put this in perspective, just two years ago, this rate was a mere 1.8%.

Now trailing closely behind office mortgages, multifamily CMBS has become the second most distressed category in CRE, ahead of lodging (6.5%) and retail (6.4%). Industrial properties, like warehouses, continue to exhibit resilience with a delinquency rate of only 0.6%.

Understanding Extend-and-Pretend Strategies

“Extend and pretend” is a strategy often employed to address delinquent loans. For instance, the $1.04 billion mortgage on 1211 Avenue of the Americas—a prominent office tower in Midtown Manhattan—became delinquent in August. Originally financed in 2015, this mortgage was due to balloon in August 2025. However, Trepp reports that a three-year term extension has already been negotiated, effectively pushing the maturity date out to August 2028. This maneuver exemplifies the extend-and-pretend approach.

Loans can be deemed “cured”—and thus removed from delinquency lists—when interest payments resume, or if alternative arrangements like extensions, modifications, or forbearance deals are reached. The complexity of these strategies often leads to deferral of eventual losses.

For example, the $335 million mortgage on Times Square Plaza, which had fallen delinquent, was “cured” in August through a forbearance agreement involving a two-year respite in payments.

Who Bears the Risk of CRE Mortgages?

Understanding who is accountable for these delinquent mortgages is crucial. Office mortgage debt is predominantly dispersed among global investors through CMBS and collateralized loan obligations (CLOs), with limited direct exposure for banks. Although some banks have reported significant write-downs and losses, many have offloaded bad loans to institutional investors at steep discounts.

On the other hand, multifamily mortgages constitute the largest segment of CRE debt, with $2.2 trillion outstanding—accounting for 45% of the total $4.8 trillion in CRE debt as reported by the Mortgage Bankers Association. A significant portion of this debt is held or guaranteed by U.S. government entities like Fannie Mae and Freddie Mac, leaving taxpayers ultimately on the hook for over half of multifamily CRE debt.

Conclusion: A Systemic Risk?

The comparatively limited exposure of U.S. banks to CRE mortgages indicates that the current situation is unlikely to pose a systemic risk to the banking sector. While losses are primarily affecting investors and government entities, the Federal Reserve is likely to allow market forces to rectify the situation organically.

As the CRE market navigates this challenging landscape, the conversation around forbearance strategies and delinquency rates remains pivotal to understanding future developments in the real estate sector.

Supporting WOLF STREET

If you’ve found this analysis insightful and wish to support independent journalism, consider making a donation. Your contributions are immensely appreciated!

For daily insights on market trends, stay tuned for updates from Chris Vermeulen, Chief Investment Officer at TheTechnicalTraders.com.